On-Demand Webinar: Building-Level Energy Savings | Measurabl Optimize

Watch the on-demand webinar recording to learn how real estate teams can use utility interval data to uncover energy savings, reduce waste, and improve portfolio performance without new hardware.

How Utility Interval Data Helps Real Estate Teams Find Energy Savings Faster

Energy costs are rising across commercial real estate, and so is the pressure to operate buildings more efficiently. For owners, operators, and asset managers, this

Measurabl Achieves PCAF Accreditation

Offering Financed Emissions Reporting Aligned with Leading Industry Standard We’re excited to announce that Measurabl has joined the Partnership for Carbon Accounting Financials (PCAF) Accredited

The ROI of Decarbonisation: Top Takeaways from MIPIM 2026

Highlights from MIPIM’s Road to Zero Stage on how real estate leaders are delivering decarbonisation across active, income-generating buildings Last month, we joined industry leaders

From Data to Performance: Measurabl Joins REALPAC to Advance Sustainability Data in Canadian Real Estate

In Canada, sustainability data is becoming essential to real estate performance. As energy costs rise, regulation evolves, and investor scrutiny increases, owners and operators need

Measurabl Receives Global ESG Compliancy Award at MIPIM 2026

Measurabl was honored to receive the Global ESG Compliancy Award presented during MIPIM 2026 in Cannes! The award recognizes solutions that help organizations meet increasingly

Why Sustainability Data Assurance Is Becoming a Competitive Advantage

There’s a concept in economics called “threshold effects”—the point where gradual changes suddenly become categorical differences. You see this everywhere: how a credit score of

Measurabl Achieves ISO 14064-3: Third Party Assurance for GHG Emissions Metrics

Measurabl has officially received ISO 14064-3 certification from Lloyd’s Register Quality Assurance (LRQA), a globally accredited body for greenhouse gas (GHG) verification. This achievement affirms

New Integration: Automating UK Electricity and Gas Data for ESG Reporting

Measurabl has launched a new integration with Perse, enabling automated electricity and gas data collection across the UK. Through Perse energy data integration, monthly utility

Energy Benchmarking Webinar Recap: What Real Estate Teams Need for 2026 Ordinance Filing

Energy benchmarking and ordinance filing used to feel straightforward: benchmark annually, submit once, move on. That is not the world we are in anymore. In

Energy Benchmarking & Ordinance Filing for Real Estate

Energy benchmarking and ordinance compliance now span 40+ jurisdictions across North America. Learn what’s changed this filing season and how real estate teams can reduce risk.

My Commitment as CEO of Measurabl: Where Customer Outcomes Matter

As CEO of Measurabl, Maureen Waters shares a clear commitment to customer outcomes, trusted sustainability data, and decision-driven real estate performance.

S&P Global & Measurabl Strengthen GRESB Verification

We’re excited to announce an expanded partnership with S&P Global to offer independent GRESB verification services as real estate teams prepare for the upcoming reporting

Powering Compliance, Quality & Performance Webinar by Measurabl

Advancing Real Estate Sustainability from Data Collection to Decision-Grade Performance: What’s Live & What You Can Look Forward to with Measurabl This post recaps a

Measurabl Names Maureen Waters CEO for Customer-Focused Growth

Maureen Waters tapped to advance Measurabl’s mission to be the global source of truth for sustainability data San Diego, CA — December 16, 2025 —

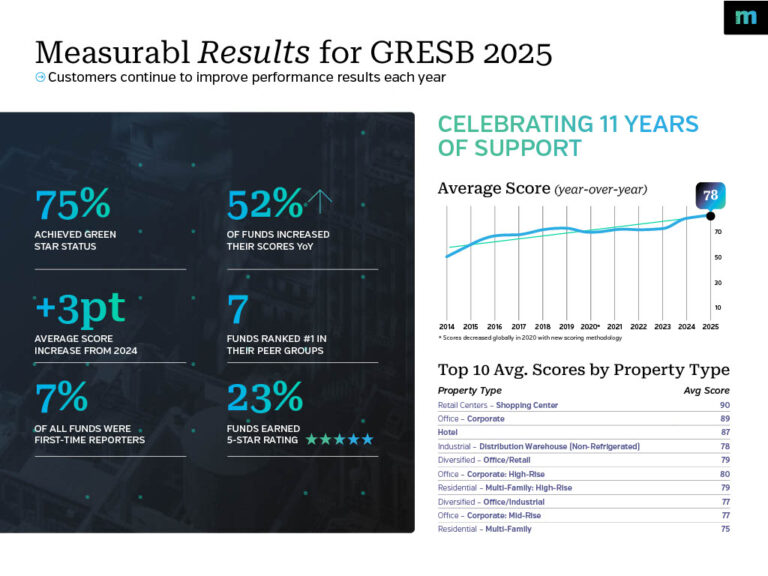

Measurabl Results for GRESB 2025 + How to Prepare for 2026

For more than a decade, Measurabl customers have trusted our platform to support their GRESB reporting and strengthen the quality of their sustainability data. This

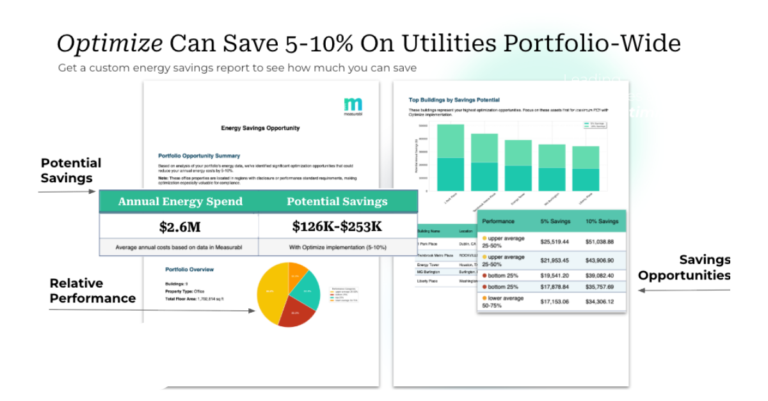

Webinar Replay – The ROI of Sustainability: How Real-Time Building Insights with Measurabl Optimize Drive Sustainability Performance

From quick wins to lasting value—what real operators taught us about energy savings through Measurabl’s Optimize At our recent ROI of Sustainability webinar, leaders from

USGBC California Selects Measurabl as Technology Partner for Real Estate Sustainability Benchmarking

Measurabl delivers a free solution to help California’s real estate owners, operators, and investors benchmark environmental performance, ensure compliance, and improve data quality SAN DIEGO,