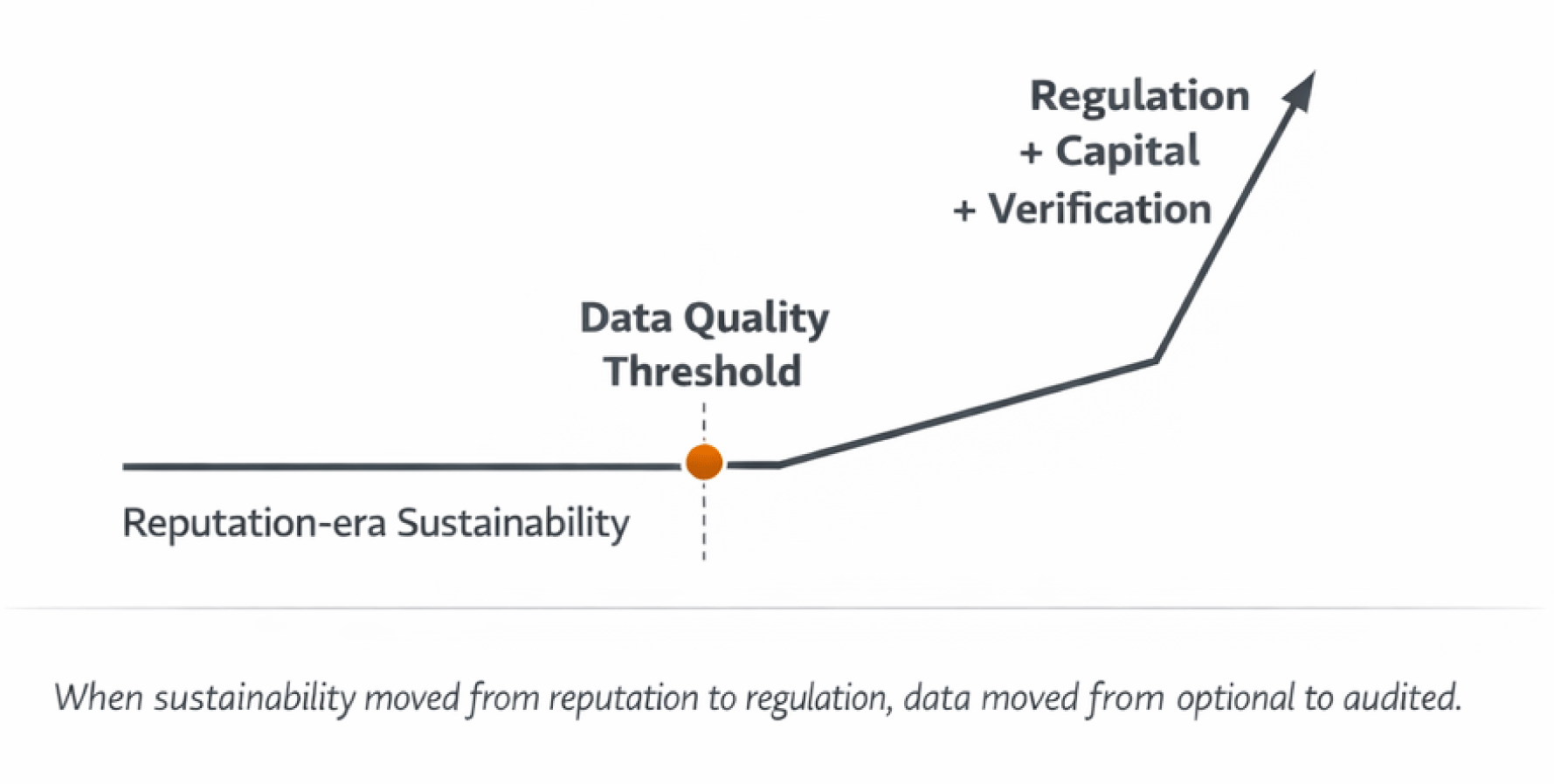

There’s a concept in economics called “threshold effects”—the point where gradual changes suddenly become categorical differences. You see this everywhere: how a credit score of 699 gets you rejected while 700 gets approved, or how a stock stays flat for months before breaking resistance and doubling overnight.

Real estate sustainability data just hit its threshold moment.

For years, sustainability metrics lived in a comfortable middle ground. Companies collected energy usage, tracked carbon emissions, and filed the occasional sustainability report. The data was important enough to measure but didn’t need the same rigor as financial statements. Rough estimates worked fine.

That era ended faster than most people realized. Between new carbon regulations, lender requirements, and investor demands for verifiable climate commitments, “rough estimates” now mean compliance failures, stalled financing, and eroded asset values. The companies that recognized this shift early are already building defensible competitive advantages. The ones still treating sustainability data as a nice-to-have are about to discover what threshold effects mean.

Measurabl saw this coming. The company built its platform on integrity, transparency, and trust from the beginning. Their recent ISAE 3000 Type II accreditation isn’t a pivot to meet new demands—it’s validation of principles that have guided their approach since day one, now supporting 23 billion square feet of real estate across 90+ countries.

The question isn’t whether data quality will become non-negotiable. It already has. The question is whether the companies in your portfolio have the data infrastructure and governance practices in place to meet this new reality, or whether they need to partner with certified data management platforms that can provide these capabilities.

The Half-Trusted Era Is Over

Sustainability data used to occupy a peculiar space in corporate reporting. Companies tracked it because it seemed responsible, investors asked about it during due diligence, and regulators occasionally requested it for compliance checks. But nobody treated it with the same precision they applied to revenue recognition or balance sheet reconciliations.

This half-trusted approach made sense when sustainability was primarily about reputation management. Scores influenced some investment decisions, green certifications provided marketing value, and carbon footprint reports demonstrated good corporate citizenship. The stakes were manageable, and the standards were forgiving.

Three forces changed everything simultaneously.

Regulations Got Teeth

Building performance standards across major cities now carry real penalties. New York’s Local Law 97 can fine large buildings $268 per metric ton of excess carbon emissions. California’s benchmarking requirements affect hundreds of thousands of properties, with non-compliance resulting in escalating fines and public disclosure of violations.

These aren’t distant threats. GRESB 2025 results show that companies with strong data management systems achieved average scores of 78 points, with 52% improving year-over-year. The 2026 assessment updates will emphasize “credible, well-documented data” for net-zero targets and require “complete, accurate asset-level performance data” over policy statements alone.

Capital Markets Shifted Standards

Lenders and investors stopped accepting sustainability metrics at face value. Green loan programs from HUD and Fannie Mae require verified energy performance data. Insurance companies factor climate risk assessments into underwriting decisions. Real estate investment trusts face increasing pressure to provide defensible sustainability disclosures to institutional investors.

The European Union’s Sustainable Finance Disclosure Regulation (SFDR) exemplifies this shift. Funds managing European capital must provide detailed sustainability metrics with clear methodologies and supporting documentation. Similar requirements are spreading globally as investors demand proof, not promises.

Technology Made Precision Possible

Modern platforms can now process millions of data points with audit-level accuracy. Machine learning models identify outliers and inconsistencies that manual reviews would miss. Automated workflows track changes from initial data ingestion through final reports, creating clear audit trails for regulators and investors.

ISAE 3000 Type II: The New Gold Standard

Most real estate professionals haven’t heard of ISAE 3000 Type II yet. They will soon.

The International Standard on Assurance Engagements (ISAE) 3000 establishes principles for assurance services beyond traditional financial audits. Type II certifications require independent auditors to evaluate both the design and operating effectiveness of an organization’s control systems over extended periods.

For sustainability data, this means rigorous validation of how companies collect, process, and report environmental metrics. Independent auditors examine data sources, review calculation methodologies, test control procedures, and verify output accuracy. The certification confirms that sustainability workflows meet the same standards applied to financial reporting.

Measurabl’s ISAE 3000 Type II accreditation validates several critical capabilities:

Emissions data aligned to assurance principles: Every carbon calculation follows established methodologies with clear documentation of assumptions, boundaries, and sources. This eliminates the guesswork that has historically plagued emissions reporting.

Transparent, traceable processes: Complete audit trails track data from initial utility bills and meter readings through final sustainability reports. Auditors can verify the source and transformation of every data point.

Elevated credibility with stakeholders: Investors, lenders, and regulators increasingly expect independent verification of sustainability claims. ISAE 3000 certification provides that third-party validation.

This certification joins Measurabl’s existing SOC 2 Type II, and ISO 14064 credentials to create a comprehensive assurance framework. Together, these standards process hundreds of millions of data points daily across the platform’s 37% market share among top global asset managers.

The Complete Certification Stack: How Standards Work Together

Understanding individual certifications misses the bigger picture. Real data integrity requires multiple complementary standards working in concert, each addressing different aspects of the data lifecycle.

SOC 2 Type II: Processing Integrity Foundation

Service Organization Control (SOC) 2 reports evaluate controls relevant to security, availability, processing integrity, confidentiality, and privacy. Type II assessments examine control effectiveness over time, typically six to twelve months.

For sustainability data, SOC 2 processing integrity controls ensure accurate, consistent, and timely data handling. This means utility bill uploads don’t corrupt during transmission, energy calculations follow consistent formulas, and report generation produces identical results when run multiple times with the same inputs.

These controls become critical when platforms handle diverse data sources. Energy bills from different utilities use varying formats and units. Water consumption reports may include different service categories. Waste haulers provide pickup weights in different measurement systems. SOC 2 controls ensure these variations don’t introduce calculation errors or reporting inconsistencies.

ISO 14064: Greenhouse Gas Accounting Standards

ISO 14064 provides international standards for greenhouse gas emissions quantification, monitoring, reporting, and verification. Part 1 addresses organizational-level emissions inventories. Part 2 covers emissions reduction projects. Part 3 establishes validation and verification requirements.

This standard becomes essential as carbon accounting grows more complex. Scope 1 emissions from on-site fuel combustion require different calculation methods than Scope 2 emissions from purchased electricity. Scope 3 emissions from waste disposal, business travel, and supply chain activities introduce additional methodological challenges.

ISO 14064 compliance ensures consistent boundaries, accurate emission factors, and appropriate uncertainty assessments. This consistency enables meaningful comparisons across properties, portfolios, and time periods while supporting regulatory requirements and voluntary reporting frameworks.

ISO 27001: Information Security Framework

ISO 27001 establishes information security management systems (ISMS) with systematic approaches to managing sensitive information. The standard requires regular risk assessments, security controls implementation, and continuous improvement processes.

Real estate sustainability data includes surprisingly sensitive information. Utility bills reveal occupancy patterns and operational details. Energy consumption data can indicate lease renewals, tenant departures, and operational changes before they become public. Building performance metrics may affect property valuations and investment decisions.

ISO 27001 certification confirms that this information receives appropriate protection throughout its lifecycle. Access controls limit data visibility to authorized personnel. Encryption protects data in transit and at rest. Backup and recovery procedures ensure availability during system failures or security incidents.

Real Portfolio Impact: Beyond Compliance Theater

Certifications matter because they enable capabilities that weren’t possible with less rigorous data management. Companies with comprehensive assurance frameworks achieve measurable advantages across multiple business functions.

Enhanced GRESB Performance

GRESB provides the clearest evidence of certification value. Measurabl customers achieved remarkable 2025 results: 75% earned Green Star status, 16 funds received 5-Star ratings (with 12 maintaining their status from 2024), and 7 funds ranked number one in their peer groups.

These results reflect systematic data quality improvements enabled by certified workflows. Enhanced Data Manager reviews catch inconsistencies before submission deadlines and identifies missing data points that would reduce scores. Portfolio Trends highlight unusual patterns that require investigation.

The 2026 GRESB assessment updates will emphasize evidence over policies. Organizations must demonstrate actual implementation through audits, efficiency projects, and certifications rather than just describing their sustainability strategies. Certified data management systems provide the documentation and verification capabilities these requirements demand.

Streamlined Due Diligence

Property acquisitions, financing arrangements, and insurance renewals increasingly require detailed sustainability data analysis. Traditional due diligence processes involved manual data collection, spreadsheet calculations, and time-consuming verification procedures that often delayed transactions.

Measurabl’s Diligence tool demonstrates how certified data transforms this process. Enter a property address, and machine learning models trained on 22 billion square feet provide instant energy and carbon estimates, climate hazard assessments, certification status, and regulatory compliance requirements.

This capability relies on data quality standards that ensure model accuracy. Incomplete or inconsistent training data would produce unreliable predictions. Certified workflows provide the data integrity necessary for automated analysis tools that deliver actionable insights in minutes rather than weeks.

Optimized Decarbonization Planning

Net-zero commitments require detailed emissions baselines, reduction pathway analysis, and progress tracking systems. These capabilities depend on data accuracy and consistency that manual processes can’t reliably deliver.

Certified platforms enable sophisticated scenario modeling against frameworks like CRREM pathways. Property managers can evaluate different retrofit strategies, compare efficiency investment options, and optimize capital expenditure timing to meet emissions reduction targets while maximizing financial returns.

The calculations involved are complex. Energy efficiency improvements affect multiple building systems simultaneously. Renewable energy installations require weather pattern analysis and grid interconnection assessments. Carbon accounting must reflect actual operational changes rather than theoretical projections.

Looking Forward: The Data Quality Imperative

The real estate industry’s sustainability data requirements will continue intensifying as regulations mature and stakeholder expectations rise. Organizations that establish strong data management capabilities now will maintain competitive advantages as these trends accelerate.

GRESB’s 2026 assessment updates preview coming changes across the industry. Emphasis on verified performance data over policy descriptions reflects investor demands for measurable results. Requirements for net-zero pathway documentation and climate risk quantification will become standard expectations rather than voluntary disclosures.

European regulations like SFDR and CSRD provide models for requirements that will likely spread to other markets. The EU Taxonomy for sustainable activities establishes technical screening criteria that require detailed performance data for compliance verification. Similar frameworks are under development in multiple jurisdictions.

Carbon pricing mechanisms will create direct financial incentives for accurate emissions measurement and reduction. Cap-and-trade programs require verified emissions data for compliance and trading activities. Carbon tax systems depend on accurate reporting for assessment and collection procedures.

Technology developments will enable more sophisticated analysis capabilities that depend on high-quality data inputs. Artificial intelligence applications require large, consistent datasets for training and validation. Digital twin models need accurate operational data to provide useful optimization recommendations. Predictive maintenance systems depend on reliable sensor data to identify equipment issues before failures occur.

The moment has arrived. Companies can choose to meet rising data quality expectations proactively or reactively. The economic advantages increasingly favor early adopters who build comprehensive data management capabilities before external pressures force rapid implementation.

Measurabl’s certification achievements, ISAE 3000 Type II, SOC 2 Type II, ISO 27001, and ISO 14064; demonstrate what comprehensive data assurance looks like in practice. These standards provide the foundation for confident sustainability reporting, efficient regulatory compliance, and strategic decision-making that creates lasting competitive advantages.

Conclusion: Building Tomorrow’s Infrastructure Now

The real estate industry’s data quality threshold moment is here. Companies that recognize this shift and invest in comprehensive assurance frameworks now will maintain competitive advantages as requirements continue intensifying. Those that delay will face increasing compliance costs, financing challenges, and operational inefficiencies as the market leaves them behind.

Measurabl’s achievement of ISAE 3000 Type II certification alongside existing SOC 2, ISO 27001, and ISO 14064 credentials demonstrates what comprehensive data assurance looks like in practice. These aren’t marketing achievements—they’re operational capabilities that process hundreds of millions of data points daily across 22 billion square feet of global real estate assets.

Certified systems deliver measurable returns through improved GRESB scores, reduced financing costs, enhanced operational efficiency, and protected asset values. As regulations mature and stakeholder expectations rise, these advantages will compound into lasting competitive differentiation.

The question isn’t whether sustainability data quality will become non-negotiable. It already has. The question is whether your organization will lead or follow as the industry transforms around this new reality.